As you probably know, the stock market is experiencing the first bear market (20% correction in the S&P 500) since 2009. Although we have had a historic stock market run over the past 10 years, it doesn’t make these drops any easier.

I certainly don’t want to make light of the situation, but there are some financial planning strategies that you may want to consider to take advantage of this stock market decline.

Most importantly, I hope that you and your family stay healthy during these very tough times.

Roth IRA Conversion

If you are considering a Roth IRA conversion, this may be the perfect opportunity for you. A Roth conversion is the process of moving money from a pre-tax IRA or 401(k) into a Roth account. As a result of the Roth conversion, you will need to pay both Federal and state taxes on the IRA withdrawal in the year of the conversion. The big benefit of the Roth conversion is that the Roth money will grow tax-free for the rest of your life. The more that the Roth account grows, the bigger the benefit.

Why now? Roth conversions are ideal when the market is down because prospects for growth are higher. Also, you can convert more of an investment now, as a result of the lower prices. As of this writing, Apple shares are currently trading at $252 per share. You could convert 100 shares of Apple stock for $25,200. Prior to this recent stock market drop it would have cost you closer to $31,000 to convert 100 shares of Apple. This stock market drop now allows you to convert more of your investments and have a lower tax bill. Also, when the market rebounds, all the future growth of the investments will be tax-free.

IRA or Roth IRA Contribution

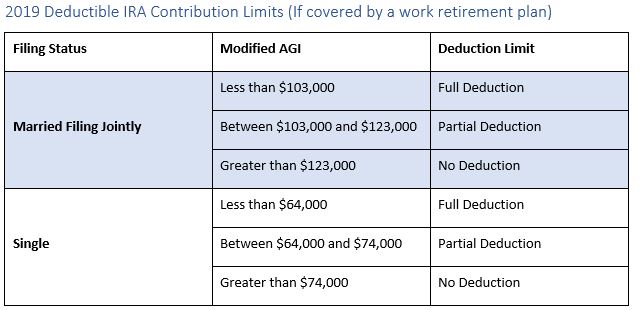

As tax time grows closer, now may be an ideal time to make your 2019 contribution to an IRA or Roth IRA. For 2019, a person under the age of 50 can contribute $6,000 to an IRA and those aged 50 or over are able to contribute $7,000 to an IRA (Source: IRS). However, there are income restrictions that may hamper your ability to contribute to a Roth IRA or take a deduction for a Traditional IRA. See below for those restrictions:

Source: IRS

Source: IRS

As a reminder, you can make an IRA contribution up to your tax filing deadline.

Why now? Like a Roth conversion,now may be a good time to make an IRA contribution when the market is down. If you have money sitting in a checking or savings account earning nothing (or losing nothing now) you may be able to put this money into an IRA and attempt to put money to work while the stock market is lower.

Tax-Loss Selling

If you have an after-tax brokerage account, there is a good chance that you have investments with large capital gains. I work with clients that have bought stocks that have doubled or tripled over the past 5 to 10 years as a result of a very strong stock market. Obviously, this is a great thing but can add risk to a portfolio as certain positions become very large. The trouble is that if a person sells these stocks with large gains, they will have a large tax bill. On the other side of things, if you have bought an investment recently, there is a good chance that you have some losses as well.

Why Now? This may be a good opportunity to sell some of the big winners that you have wanted to get rid of without facing as big of a tax-gain. Selling losers may allow you to offset some of those gains and potentially allow you to offset some income if you don’t have any gains to offset.

I’m certainly not advocating to sell all your investments and move to cash. However, this may be a good opportunity to sell some of your big winners or losers and move to a more diversified portfolio.

Increase 401(k)/403(b) Contributions

If you are still working and contributing to a 401(k) these market drops create an opportunity to buy more investments at lower prices. If you aren’t maxing out your 401(k)/403(b) this may be a good opportunity to raise your contributions and get more money working for you. If you are planning on maxing out your 401(k)/403(b) for the year, you may raise contributions now so that you max out earlier in the year. In 2020, a person can contribute up to $19,500 to a 401(k)/403(b), and if 50 or over, an additional $6,500 per year into catch-up contributions.

Why now? The key to long-term investment outperformance is to buy low and sell high. We all know this; however, it is a little harder to do in real life. Like some of the other strategies that I discussed, raising 401(k) contributions allows you to purchase more investments while stocks are lower. Certainly, stocks can still go down, but compared to where we were about a month ago, stocks are on sale. Buying low helps your account rebound quicker when the market does move higher.

Need Additional Help?

RetireMitten Financial LLC is a fee-only financial planning firm based in Milford, MI. We specialize in helping families live a stress-free retirement. Let us help you create your retirement paycheck. Schedule a complimentary meeting below.

Image by Free-Photos from Pixabay

Great strategies for a market correction! Diversifying investments reduces risk, while a contingency fund provides a safety net. Regularly rebalancing the portfolio helps maintain desired allocations. Remember, a long-term perspective is key. Thanks for sharing these valuable insights!